Where Are We? Part 1: Bubbles, Bubbles, Toils, and Troubles

Carlota Perez helps us understand why bubbles are good for technology—but do they mean we're in a 20-year financial frenzy?

This is the first installment in “Where Are We?”, an ongoing series by Annika Lewis and David Phelps that breaks down economic theorists to try to figure out where exactly we are in a cycle.

(Also, you should subscribe to Annika’s great Medium here.)

For this first stab at determining just when and where we are, we’re looking at 2002’s Technological Revolutions and Financial Capital, by Carlota Perez. One of the great economists of our time, Perez is a leading thinker on technology and socio-economic development. Her book outlines a four-phased financial cycle depicting the archetypical sequence of capital deployment and market traction for a major technological revolution. In this post, we’ll dig into Perez’s cycle and discuss where we sit today in 2021.

Perez’s Cycle: A Quick Overview

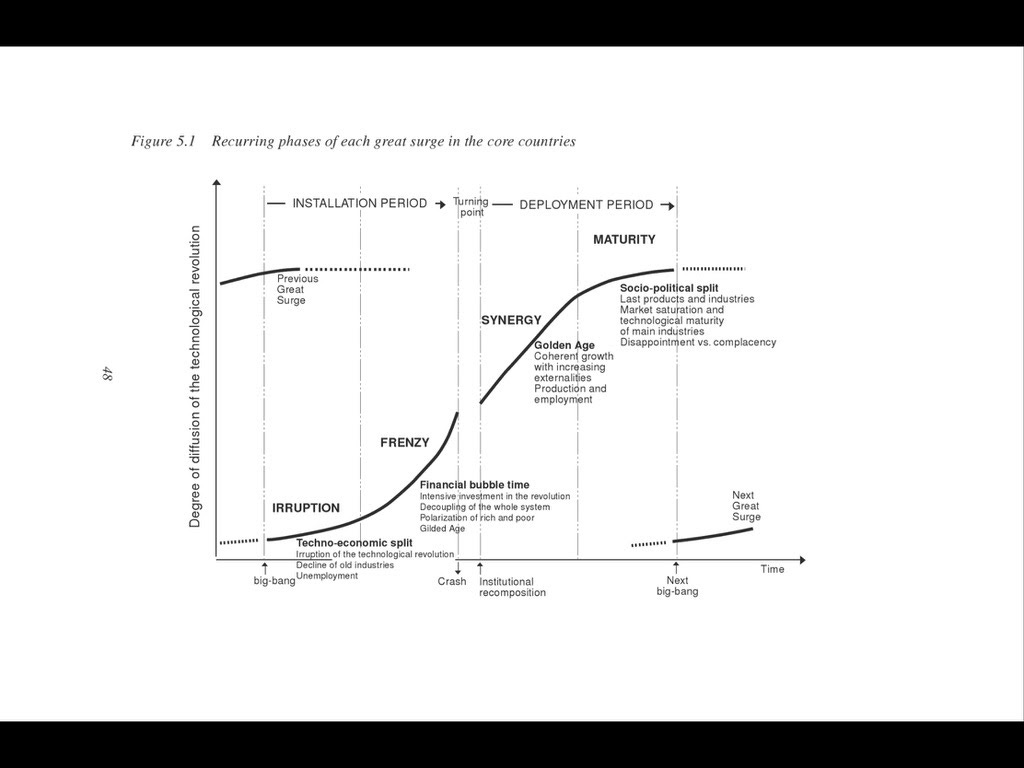

In Technological Revolutions and Financial Capital, Perez outlines an archetypical four-phased financial cycle. This cycle is intended to roughly map one-to-one to each major technological revolution, as well as the capital deployment that drives it.

The four phases—paraphrased and simplified a bit—are:

Irruption — Decline of old industries, and the new tech just starting off

Frenzy — Intensive investment in the new tech, and a financial bubble

Synergy — Growth as the new tech goes mainstream, a prosperous time

Maturity — Last products in deployment, saturation, and standardization

Perez suggests the full cycle lasts roughly fifty years.

It is also important to note that there’s a ‘Turning Point’ after the Frenzy phase—a financial bubble-induced crash and recovery—before moving into the Synergy phase.

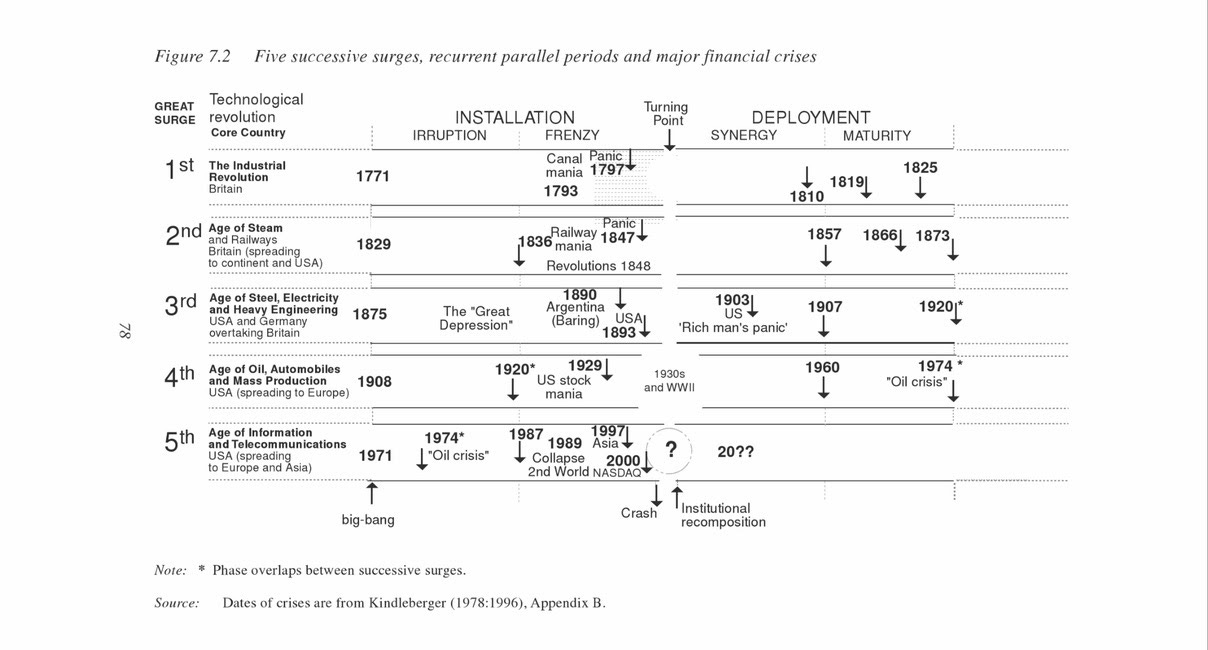

Perez then takes this four-phased cycle, and overlays it with five specific ‘great surges’ in history, major technological revolutions that have occurred in the past 500 years:

But let’s try an exercise here—what do we see if we look at Perez’s two seminal charts illustrating the four stages of technological development without the benefit of her commentary?

Let’s start with the easiest way of telling this story.

Technological development is slow at first in the “Irruption” stage: on the production side, not that many people are working on it, and on the financial side, not that many people believe in it. But its rate of acceleration is high, and the technology undergoes exponential growth in the “Frenzy” phase as money starts pouring in. Since new technologies seem to develop in S-curves, however—presumably meaning that once they’ve overtaken the earth, they don’t have much room to expand—these technologies inevitably reach an inflection point where they begin to decelerate even as they continue to grow. This deceleration is devastating for capital, which had priced in a continued rate of growth, so bubbles collapse right at this inflection point; quite simply, decelerating technologies can’t fulfill the high expectations of finance. From there, new technology becomes normalized, expanding its reach to all markets until it has no room to grow. Ideas and capital go elsewhere.

That’s the simplest way of telling this story because it posits the simplest relationship between technology and finance: that old-school finance is forever reacting to new-school technologies, finally understanding the innovators a decade late, funding them excitedly based on historical performance, but wresting their money from markets when it's clear their expectations can’t be met. This story is not so different from Ray Dalio’s in The Changing World Order. Finance fuels the growth of markets, justifying higher expected rates of return that ultimately technology just can’t meet. The comedy-of-errors between backward-looking finance, which derives its rates from quants calculating past performance, and forward-looking technologies, which derive their growth from futurists building platforms for new societies, means that there’s never enough capital when technologies are new and there’s always way too much when technologies go viral. The name for that comedy-of-errors is “bubbles.”

But what if we consider a more complex telling of this tale—one in which the performance of capital isn’t only dependent on the performance of technology, but the performance of technology is also dependent on the performance of capital?

In this version of the story, bubbles may ultimately be bad for finance, but they’re very good for technology in hypercharging growth. (They’re also quite good for finance in the meantime.) We now have a question of correlation/causation. When capital flees the markets as the bubble crashes, is that because the growth of technology is at an inflection point where it starts to slow? Or is it what causes technology growth to slow?

In this version of the story, technology and finance are no longer comically at odds but tragically reinforce each other—propelling each other higher and higher until one of them makes the mistake of looking down, and a brief moment of panic sends them crashing to earth. Ultimately, they settle on a dull marriage while their offspring grows up (the “synergy” phase) and, a decade or two later, they elect for a quiet divorce.

Perez, for what it’s worth, advocates for something closer to the comedy-of-errors reading, similar to Dalio and Marx, that bubbles occur when finance misprices future growth based on past performance, and technology simply is unable to fulfill its terms. “The amount of money available to financial capital has grown larger than the set it recognizes as good opportunities,” writes Perez. “Since it has come to consider normal the huge gains from the successful new industries, it expects to get them from each and every investment and will not be satisfied with less.” There is, however, a fascinating catch: so much money gluts the market that finance must find new ways to deploy it since even in the middle of a bubble, it’s already clear that technology and production won’t transform it into the expected rate of return. So finance comes up with its own technologies of sorts to put that money to use.

“Rather than go back to funding unsophisticated production,” writes Perez, “it develops sophisticated instruments to make money out of money.” Derivatives, tokenized securities, credit default swaps, collateralized loans—these all flourish when everyone wants to get in the game but realizes the best money won’t be made off long-term investments in production capital and new technologies. Even when those technologies are the impetus for the bubble itself.

Ultimately, bubbles aren’t only good for new technologies in giving them attention and money, but are actually a sign that a technology is likely to be transformative long-term—”tulips” may be the favored metonym for bubbles, but railroads and the internet catalyzed and benefitted from some of the largest historical bubbles. Whether bubbles are good for finance, however, is a question of when you get out. For those who figure out when to get out, bubbles might be the best way of making money; then again, the point of a bubble isn’t only how high it soars and how far it drops, but how many retail investors it suck in to support its rise, only to collapse when it can’t find more takers.

So what does this all mean in the context of today?

Perez first published this framework in 2002 and, based on her five successive surges chart, suggested that at that point, post-2000 crash, we had just reached the turning point and were awaiting a major reset—after which the world would move into the new normal.

And yet, 20 years later, we very much appear to still be in a frenzy phase. Assuming that’s correct, there are two obvious scenarios one could argue to reconcile these positions:

The 2008 crash marked the end of the turning point, and we’ve since entered a new cycle

We’re still at the turning point of the previous cycle, right at the end of the frenzy period

There are compelling arguments for #1. The 2008 crisis was, by definition, spurred by the creative finance technologies that Perez refers to (mortgage-backed securities, in this specific case). One could argue that the rise of the computer in the 70’s-80’s represented the Irruption phase, the dot-com bubble represented the Frenzy and the beginning of a turning point, until it all came crashing down in 2007 and we emerged into the Synergy phase. The 2010s represented the post-crash boom when internet businesses became the norm, social media took hold, and the next generations of youth became digital-first. One might even suggest that, with the traction cryptocurrency has gained, we’re already in our second phase post-internet era, living in a crypto frenzy, and we’re awaiting the crypto turning point. In this reading, the 2010s were the Synergy / Maturity phases for Web 2.0 and the Irruption phase for Web 3.0, and we’ve now entered the frenzy stage for the latter.

Now, consider scenario #2, which argues that 2008 was not the turning point of the current age, but one of a series of crashes—2000, 2008, 2020—over the past 20 years. Consider the view that the 2008 crisis was indeed spurred by ‘creative finance’, but that this creative finance was untethered to the tech & capital reinforcing cycle outlined above. The argument here is that the cycle driving the 2008 crisis was purely a result of a hard asset (i.e., real estate) bubble, spurred initially by demand for this hard asset after the tech crash, and then maintained and accelerated via creative finance.

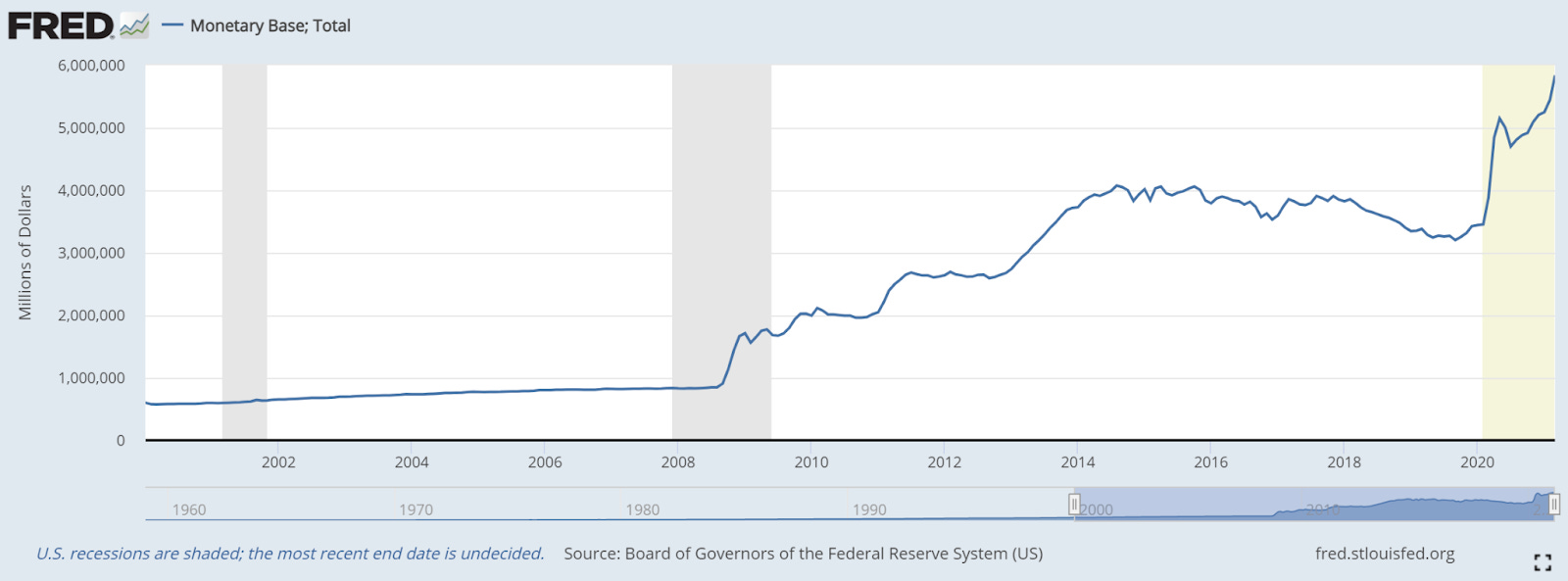

In this scenario, the 2010s are not a post-crash normalization, but rather represent the true frenzy period. The Covid-19 crisis itself did not represent the turning point; rather, the resulting low interest rates and increase in money supply have exacerbated the existing frenzy, pushing asset prices higher than before the crisis. Post-Covid, valuations have reached unprecedented levels and creative finance has come into play with SPACs, NFTs, and Wall Street Bets dominating the news in 2021. While these examples are all indicative of the frenzy on the consumer side, by far the most impactful creative finance is stemming from where people least expect it: directly from the mouth of the Federal Reserve itself. Fiscal money-printing aside, the Fed’s purchases of bonds, performed at an unprecedented scale, continue to prop up this unsustainable frenzy month after month.

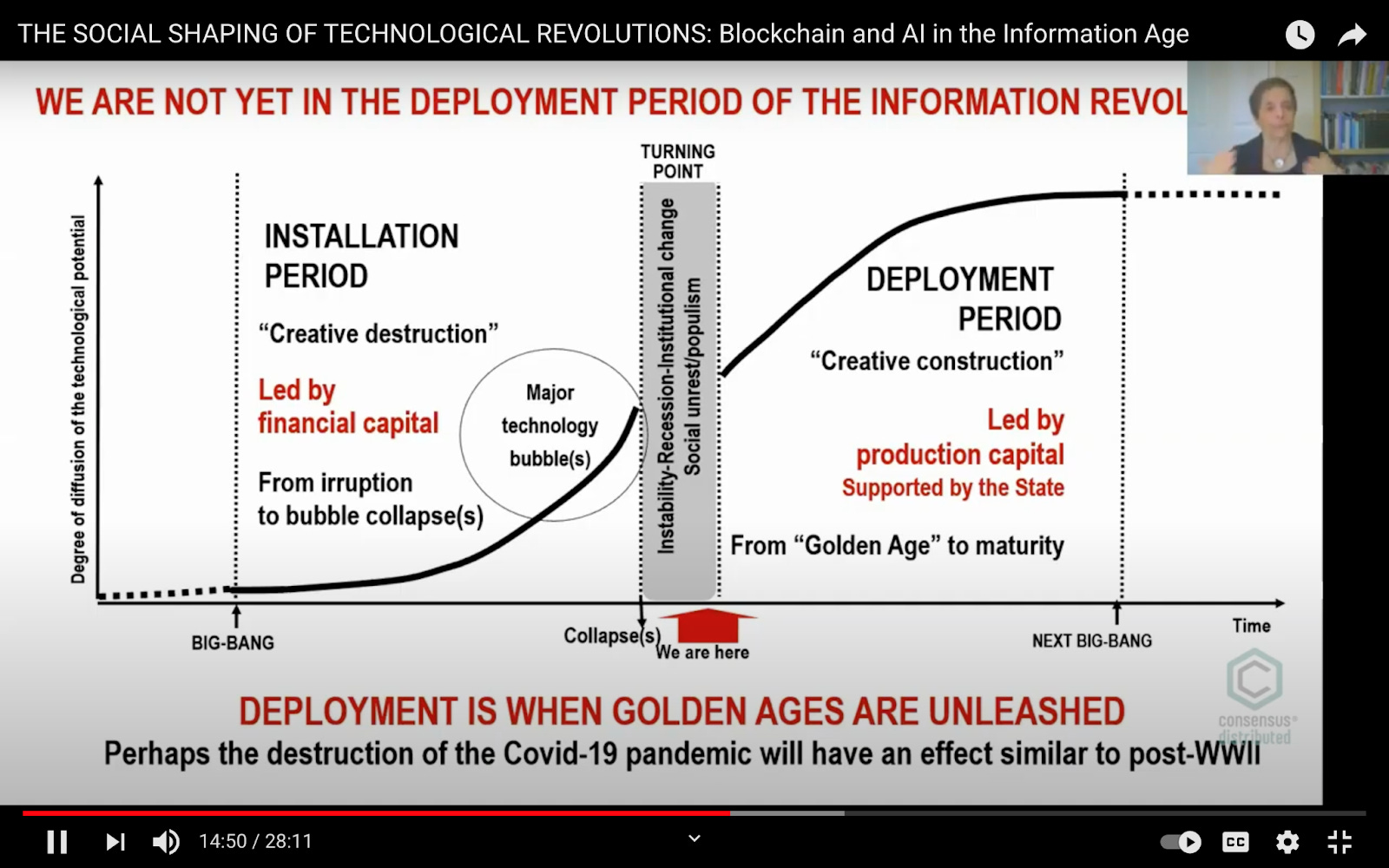

For what it’s worth, this is more or less Perez’s current view: 20 years after suggesting that we were at the turning point, Perez herself has repeatedly argued that we’re actually still there.

Here, for example, is one of her slides from 2018:

Witness how much the trends she mentions have accelerated in the past year (with the notable exception of “low investment”). The 2020 crash begins to seem like a blip; 2021 is just an amped-up 2018.

Now consider her slides from a 2020 talk for Coindesk updating her seminal chart for the 2020s:

This notion that we’re nearing the end of a turning point correlates neatly to Dalio’s cycles, which propose that devaluations through money printing are often the solution to the kind of extreme wealth economy Perez charts in the slide above. But what happens when this devaluation comes earlier than it might have (due to an unexpected pandemic), continues spurring on a frenzied stock market, and fiscal and monetary policy have little recourse when a crash finally comes?

We might register one other note of concern here too. Much of Perez’s work since Technological Revolutions and Financial Capital has worked to explain why the 2000 tech crash wasn’t the turning point it surely seemed to be at the time. In a wonderful corrective from 2009, “The Double Bubble at the Turn of the Century,” Perez posits that there are actually two types of bubbles that often accompany one another: “Major Technology Bubbles,” in which whole societies speculate on transformative technologies before they’ve generated enough capital to justify the valuations, and “Easy Liquidity Bubbles,” in which creative finance finds new ways to loan money in speculation on duller asset classes. The point is that the “opportunity pull” of the former leads finance to get creative with its own innovations through the latter “credit push” a few years later. The 2000 crash, in other words, begot the 2008 crash.

But what happens in a time where a transformative technology like cryptocurrency is also a transformative financial technology that can continue funding its own technological growth through loans in a long, virtuous cycle? We might end up with a “mother of all bubbles” scenario that could threaten the traditional world of finance as well if it became dependent on these new technologies for its own financial success.

The consolation of such froth, of course, is that it truly is good for good technology. When that technology itself represents a promise of statelessness, and the state itself continues to exhaust its own options for keeping the economy afloat, the question isn’t so much whether we’re in a bubble—but whether we’re approaching a “deployment period,” and more importantly, of just what kind of revolution we’re in.

Words by Annika Lewis and David Phelps. Drawings by Annika Lewis.